Securing a car loan is a significant part of the vehicle buying journey. When purchasing a used car, two prominent names often come up: DriveTime and CarMax. Both offer a convenient, one-stop shopping experience where you can select a vehicle and arrange financing under one roof. However, their approaches, target demographics, and financing structures differ considerably. This in-depth guide will explore the nuances of DriveTime and CarMax financing, providing you with the knowledge to choose the best option for your financial situation and driving needs.

Understanding In-House Financing

In-house financing, also known as buy-here-pay-here, means the dealership itself is the lender. This contrasts with traditional financing, where a bank, credit union, or other third-party financial institution provides the loan. For consumers, this can simplify the process, especially for those with challenged credit histories who might struggle to get approved by conventional lenders. Dealerships offering in-house financing often have more flexible underwriting criteria, focusing on your income and ability to pay rather than just your credit score.

DriveTime Financing: Tailored for Challenged Credit

DriveTime has built its business around helping individuals with poor or no credit secure auto loans. They specialize in subprime lending, making car ownership accessible to a demographic often overlooked by traditional banks. Their focus is on your current income and housing stability as indicators of your ability to repay.

Key Aspects of DriveTime Financing:

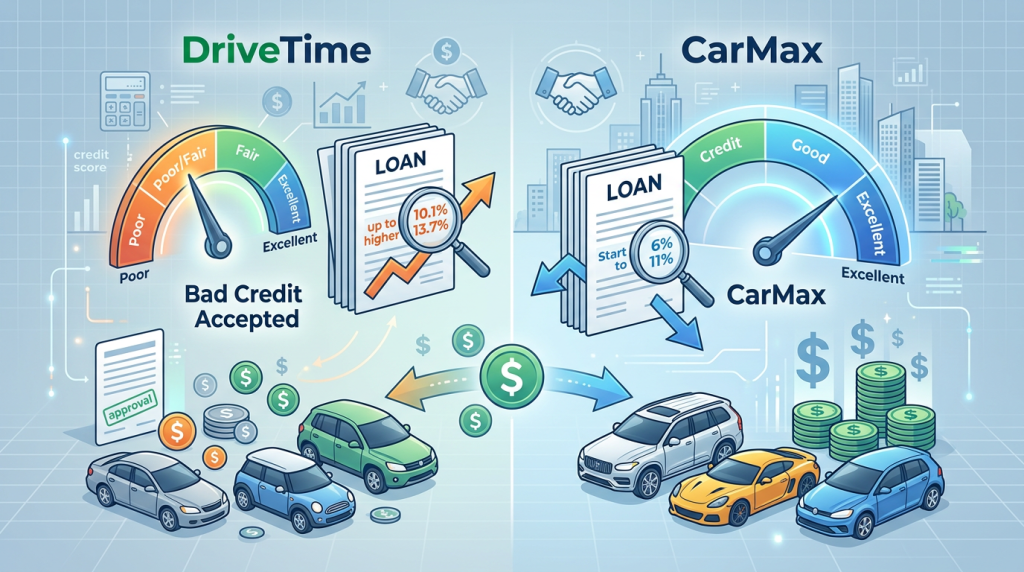

• Credit Flexibility: They are known for providing loans to those with credit scores as low as the 400s or 500s.

• Down Payment Requirement: A down payment is almost always required, and the amount will vary based on the vehicle price, your credit history, and your income. Higher down payments can reduce your monthly payments and overall interest paid.

• Higher Interest Rates (APRs): Due to the higher risk associated with subprime lending, DriveTime’s annual percentage rates (APRs) are typically significantly higher than those offered by prime lenders. Expect APRs ranging from 10% to over 25%, depending on individual circumstances.

• Shorter Loan Terms: Loan terms at DriveTime are often shorter, usually between 36 to 60 months. This can lead to higher monthly payments but also means you pay off the car faster.

• Pre-qualification: DriveTime offers a quick online pre-qualification that uses a soft credit inquiry, meaning it won’t impact your credit score. This allows you to see potential down payment requirements and estimated monthly payments before visiting the dealership.

CarMax Financing: A Broader Spectrum of Choices

CarMax positions itself as a customer-friendly used car retailer known for its no-haggle pricing and extensive inventory. While they offer their own in-house financing through CarMax Auto Finance (CAF), they also work with a wide network of third-party lenders. This hybrid approach allows them to cater to a much broader range of credit profiles, from excellent to subprime.

Key Aspects of CarMax Financing:

• Credit Spectrum: CarMax can secure financing for customers with excellent credit (700s+) down to those with credit challenges (500s-600s).

• Competitive Rates: For customers with good credit, CarMax can offer competitive APRs, often comparable to traditional banks. For those with lower scores, rates will be higher but might still be better than direct subprime lenders due to their network of lenders.

• Flexible Loan Terms: CarMax typically offers more flexible loan terms, often ranging from 36 to 72 months, or even longer in some cases. This can help adjust monthly payments to fit various budgets.

• Down Payment: A down payment is generally required, similar to other auto lenders, and its size will depend on the vehicle price, your creditworthiness, and the loan terms.

• One Application, Multiple Offers: When you apply for financing at CarMax, they submit your single application to multiple lending partners, including CAF. This can result in several loan offers, allowing you to choose the best terms.

• 30-Day Money-Back Guarantee: A standout feature of CarMax is its generous return policy, offering a 30-day (or 1,500 miles) money-back guarantee, providing significant peace of mind.

🧐 Eligibility Requirements & Approval Tips

DriveTime Eligibility:

• Income: Stable employment and verifiable income are crucial. DriveTime needs to see you can consistently make payments.

• Residency: Proof of residence is required.

• Down Payment: Be prepared for a down payment. Having a larger down payment can significantly improve your chances of approval and lower your interest rate.

CarMax Eligibility:

• Credit Score: While they work with various scores, better scores lead to better offers.

• Income & Employment: Stable income is key. They’ll look at your debt-to-income ratio.

• Debt-to-Income (DTI): Lenders prefer a DTI below 40-50%. Know your current obligations.

General Approval Tips for Both:

• Know Your Credit Score: Before you even start, pull your credit reports from all three bureaus (Experian, Equifax, TransUnion) and check for errors. Websites like Credit Karma offer free scores/reports.

• Have Documents Ready: Bring proof of income (pay stubs, bank statements), proof of residence (utility bill), and a valid driver’s license.

• Consider a Co-signer: If your credit is poor, a co-signer with good credit can significantly improve your chances of approval and potentially lower your interest rate.

• Save for a Down Payment: The more you put down, the less you need to finance, leading to lower monthly payments and less interest over the life of the loan.

• Don’t Apply Everywhere: Too many hard inquiries in a short period can hurt your credit score. Stick to a few trusted lenders or use pre-qualification tools.

📝 Step-by-Step: How to Apply (General)

Online Pre-qualification: Start using the online pre-qualification tools offered by both DriveTime and CarMax. This is a soft credit pull and gives you an initial idea of what you qualify for.

Gather Documents: Collect necessary papers: driver’s license, proof of income (pay stubs, bank statements), proof of residence (utility bill), and potentially trade-in title if applicable.

Visit Dealership: Go to your chosen dealership with your pre-qualification offer and documents.

Vehicle Selection: Choose your desired car from their inventory.

Final Application: Complete the full credit application. This will involve a hard credit pull.

Review Offers: Carefully review all financing offers, paying close attention to APR, loan term, and total cost.

Sign & Drive: Once you select the best offer, sign the paperwork and drive home in your new car.

🛠️ Optimization Tips & Industry Secrets

• Debt-to-Income Ratio (DTI) Matters: Lenders scrutinize your DTI. Try to pay down other high-interest debts before applying for an auto loan. Aim for a DTI below 40%.

• The 30% Utilization Rule: For credit cards, try to keep your credit utilization below 30% of your available credit limits. This shows responsible credit management.

• Rate Shopping Window: When applying for an auto loan, multiple hard inquiries within a 14-45 day window (depending on the credit scoring model) are often counted as a single inquiry. This means you can shop around for the best rates without significant credit damage within that period.

• Refinancing Later: If you have to take a high-APR loan with DriveTime due to poor credit, work diligently on improving your credit score. After 6-12 months of on-time payments, you may be able to refinance your loan with a traditional bank or credit union at a much lower interest rate.

• Negotiate the Out-the-Door Price: While CarMax has no-haggle pricing, you can still ensure you’re getting a fair trade-in value, if applicable. DriveTime’s prices are generally fixed, but always ensure all fees are transparent.

• Understand Add-ons: Both dealerships may offer extended warranties or service plans. Factor these into your total cost, and don’t feel pressured to buy them if they don’t fit your budget or needs. Sometimes, third-party options are more affordable.

❓ FAQ: DriveTime vs CarMax Financing

Q1: Is it harder to get approved at CarMax or DriveTime?

Generally, it is easier to get approved at DriveTime if you have bad credit, as that’s their primary market. CarMax works with a broader range of credit scores, but for the lowest credit tiers, DriveTime might be more accessible.

Q2: What’s the typical down payment for each?

Both require a down payment. At DriveTime, it can vary significantly, starting from a few hundred dollars to several thousand, largely depending on your credit and the vehicle. CarMax down payments also vary but generally follow traditional lending expectations based on credit score and vehicle price.

Q3: Can I get a 0% APR loan from either DriveTime or CarMax?

No, 0% APR offers are typically limited to new car financing deals directly from manufacturers for customers with excellent credit. Neither DriveTime nor CarMax, as used car dealerships specializing in varied credit, offer 0% APR on their loans.

Q4: Does applying for pre-qualification affect my credit score?

No, both DriveTime and CarMax use a soft credit pull for pre-qualification, which does not impact your credit score. A hard inquiry only occurs when you submit a full application for financing.

Q5: What if I get denied financing at both?

If denied, consider taking time to improve your credit score. Pay off existing debts, ensure on-time payments, and dispute any errors on your credit report. Also, exploring options with a co-signer or saving up a larger down payment could help for future attempts.

Final Opinion & Next Steps

Choosing between DriveTime and CarMax financing boils down to your individual credit situation and priorities. If your credit is significantly challenged, DriveTime may be your most viable path to car ownership, but be prepared for higher interest rates. Use their pre-qualification to understand the costs. If you have fair to good credit, or even slightly blemished credit, and value transparent, no-haggle pricing with a strong return policy, CarMax offers a compelling package and access to a wider range of lenders. Their ability to compare multiple offers can often lead to more favorable terms.

Regardless of your choice, always get pre-qualified from both (if applicable) to compare offers without affecting your credit. Read all loan documents carefully, understand the total cost of the loan (not just monthly payment), and ensure the vehicle fits your budget. Your financial future depends on making an informed decision. Drive smart!

You will be redirected to the official page.

Bad Credit Car Loans: Top 7 Cars for Easy Financing <p class='sec-title' style='line-height: normal; font-weight: normal;font-size: 16px !important; text-align: left;margin-top: 8px;margin-bottom: 0px !important;'>Drive Away Today: Best Cars for Bad Credit Car Loans & Affordable Monthly Payments</p>

Bad Credit Car Loans: Top 7 Cars for Easy Financing <p class='sec-title' style='line-height: normal; font-weight: normal;font-size: 16px !important; text-align: left;margin-top: 8px;margin-bottom: 0px !important;'>Drive Away Today: Best Cars for Bad Credit Car Loans & Affordable Monthly Payments</p>  Ultimate Guide: Finding the Best Cars Under $30,000 in 2026 <p class='sec-title' style='line-height: normal; font-weight: normal;font-size: 16px !important; text-align: left;margin-top: 8px;margin-bottom: 0px !important;'>Navigate the market with confidence. We break down the top vehicles delivering exceptional value, performance, and tech for under $30k.</p>

Ultimate Guide: Finding the Best Cars Under $30,000 in 2026 <p class='sec-title' style='line-height: normal; font-weight: normal;font-size: 16px !important; text-align: left;margin-top: 8px;margin-bottom: 0px !important;'>Navigate the market with confidence. We break down the top vehicles delivering exceptional value, performance, and tech for under $30k.</p>  Nissan Motor Acceptance: Your Path to a New Nissan <p class='sec-title' style='line-height: normal; font-weight: normal;font-size: 16px !important; text-align: left;margin-top: 8px;margin-bottom: 0px !important;'>Discover financing options, compare rates, and drive home your dream Nissan with ease and transparency.</p>

Nissan Motor Acceptance: Your Path to a New Nissan <p class='sec-title' style='line-height: normal; font-weight: normal;font-size: 16px !important; text-align: left;margin-top: 8px;margin-bottom: 0px !important;'>Discover financing options, compare rates, and drive home your dream Nissan with ease and transparency.</p>